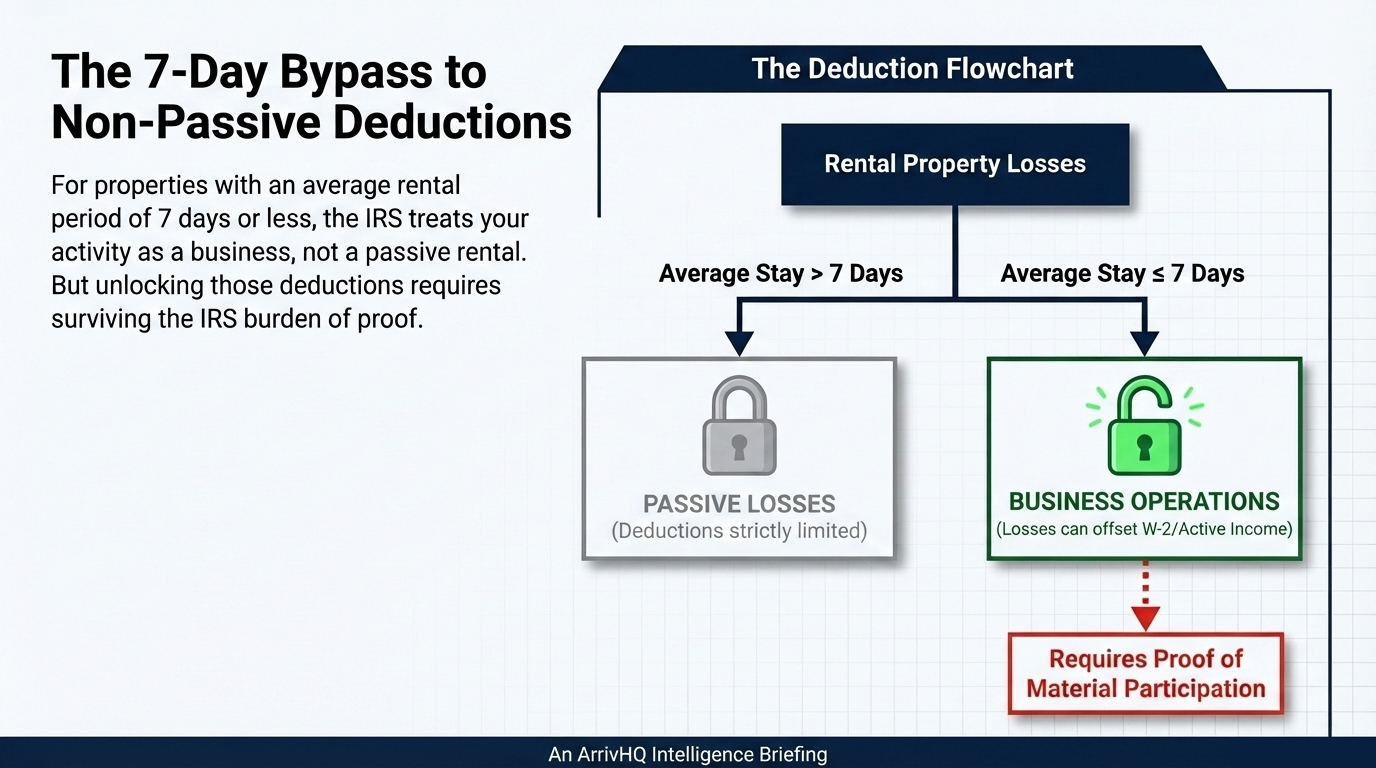

If you own a short-term rental and want to deduct losses against your other income, the IRS requires you to prove material participation. This is the single most important documentation challenge STR hosts face — and the one most get wrong.

What is material participation?

Material participation is the IRS standard for determining whether you are actively involved in running your rental business or merely a passive investor. The distinction matters because it controls whether your rental losses are passive (limited deduction) or non-passive (deductible against W-2 and other active income).

Material participation is the dividing line between passive and active tax treatment.

Material participation is the dividing line between passive and active tax treatment.

For short-term rentals — properties with an average rental period of 7 days or less — the IRS treats your activity as a business rather than a rental activity. This opens the door to material participation, but you still have to prove it.

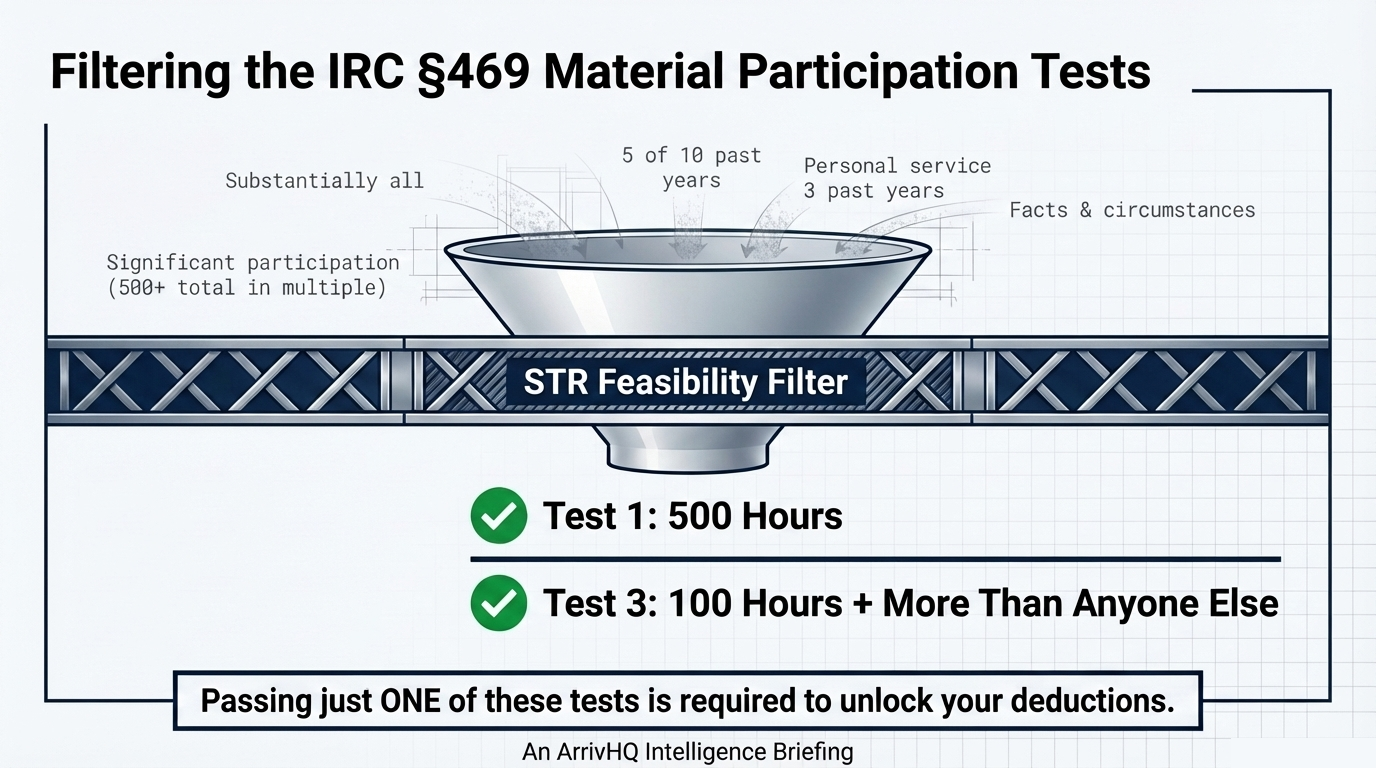

The seven IRS tests

The IRS defines seven tests for material participation (IRC §469). You only need to pass one:

- 500 hours — You participate in the activity for more than 500 hours during the tax year.

- Substantially all — Your participation constitutes substantially all participation in the activity.

- 100 hours + more than anyone else — You participate for at least 100 hours, and no other individual participates more.

- Significant participation activities — You participate in multiple activities for at least 100 hours each, totaling over 500 hours.

- 5 of 10 years — You materially participated in the activity for any 5 of the 10 preceding tax years.

- Personal service activity — The activity is a personal service activity in which you materially participated for any 3 preceding tax years.

- Facts and circumstances — Based on all facts and circumstances, you participate on a regular, continuous, and substantial basis.

For most STR hosts, Test 1 (500 hours) or Test 3 (100 hours + more than anyone else) are the paths that matter.

You only need to pass one test. For most STR hosts, Test 1 and Test 3 are the only viable paths.

You only need to pass one test. For most STR hosts, Test 1 and Test 3 are the only viable paths.

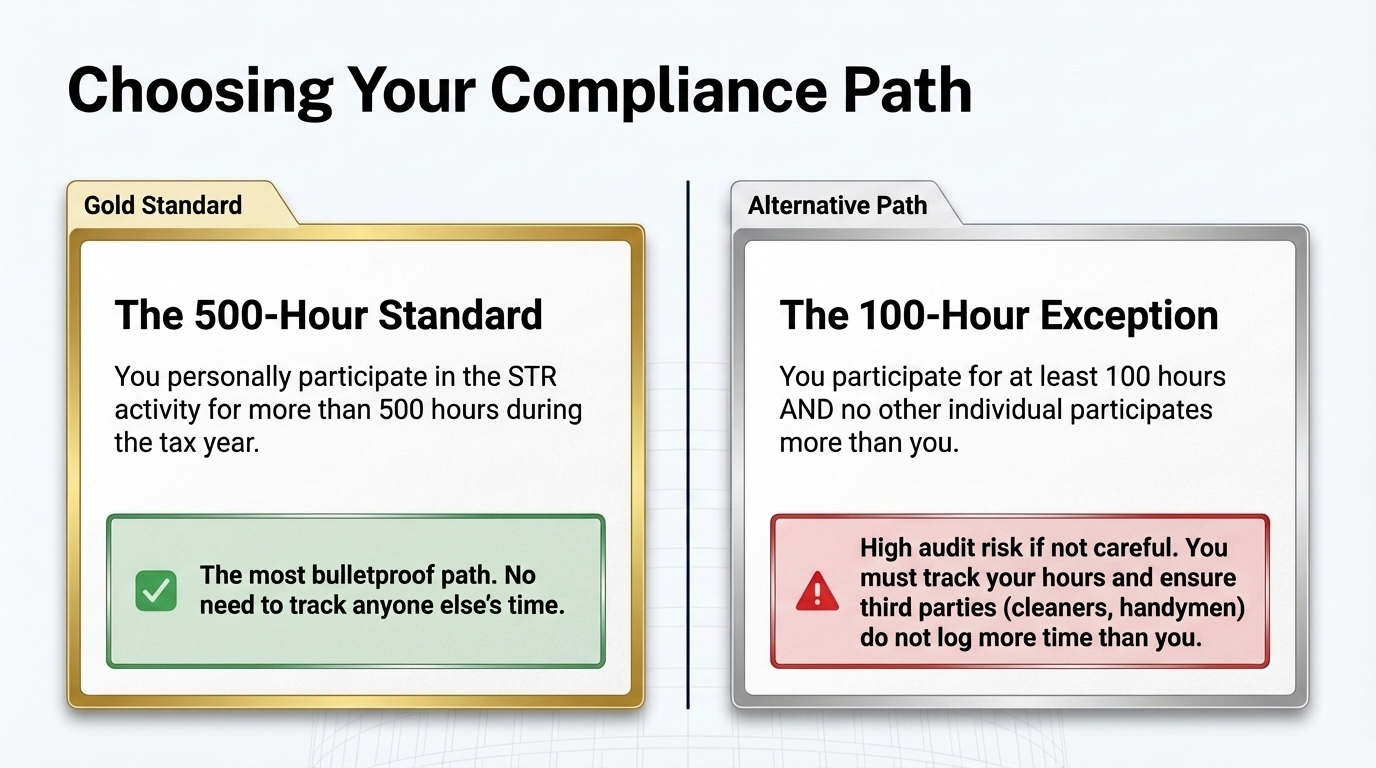

Test 1 vs. Test 3: choosing your path

The two tests have very different dynamics. Test 1 (500 hours) is high volume but zero competition — you just need to hit the number. Test 3 (100 hours) is a lower bar, but you must definitively prove you spent more time than any single cleaner, manager, or vendor.

Test 1 is a clear hurdle. Test 3 is a race — you must outpace every individual who works on your property.

Test 1 is a clear hurdle. Test 3 is a race — you must outpace every individual who works on your property.

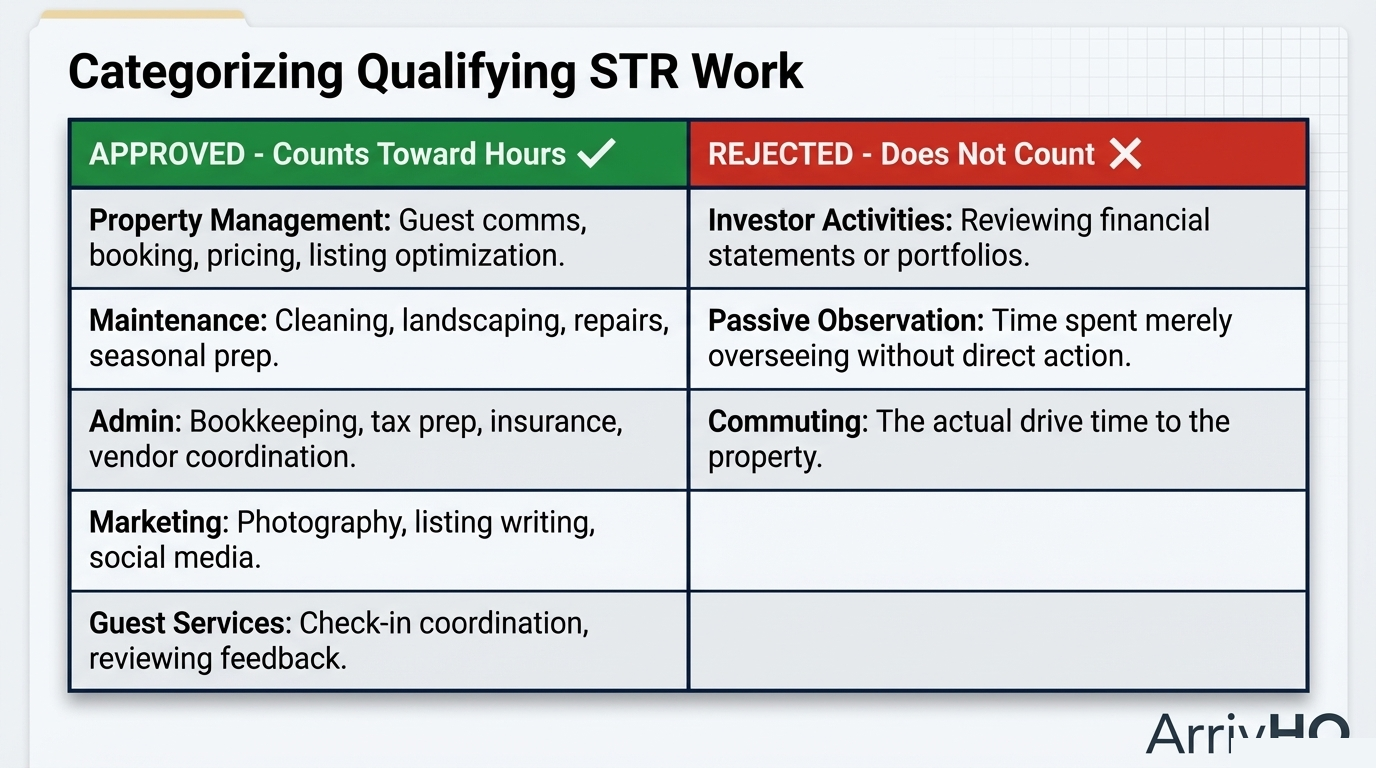

What counts as qualifying work?

Not all time spent on your STR counts toward material participation. The IRS recognizes:

- Property management — guest communication, booking management, pricing adjustments, listing optimization

- Maintenance and repairs — cleaning, landscaping, fixing appliances, seasonal preparation

- Administrative work — bookkeeping, tax preparation, insurance management, vendor coordination

- Marketing — photography, writing listings, social media promotion

- Guest services — check-in coordination, responding to issues, reviewing feedback

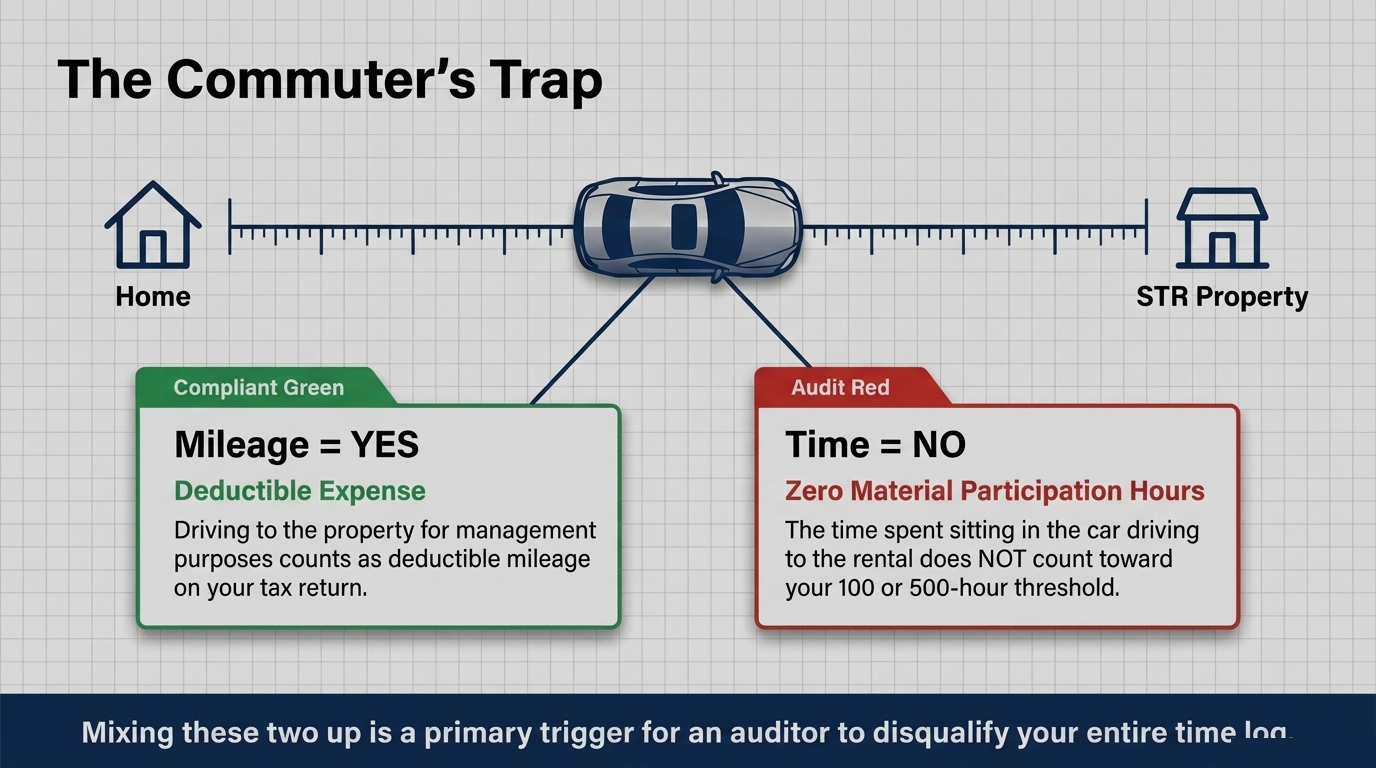

What does not count: investor-type activities like reviewing financial statements, time spent as a passive observer, and commute time (though driving to the property for management purposes counts as mileage, the drive itself is not material participation time).

The IRS draws a clear line between operational work and investor activities.

The IRS draws a clear line between operational work and investor activities.

Driving to your property counts as deductible mileage — but the time behind the wheel is zero material participation hours.

Driving to your property counts as deductible mileage — but the time behind the wheel is zero material participation hours.

How to document your hours

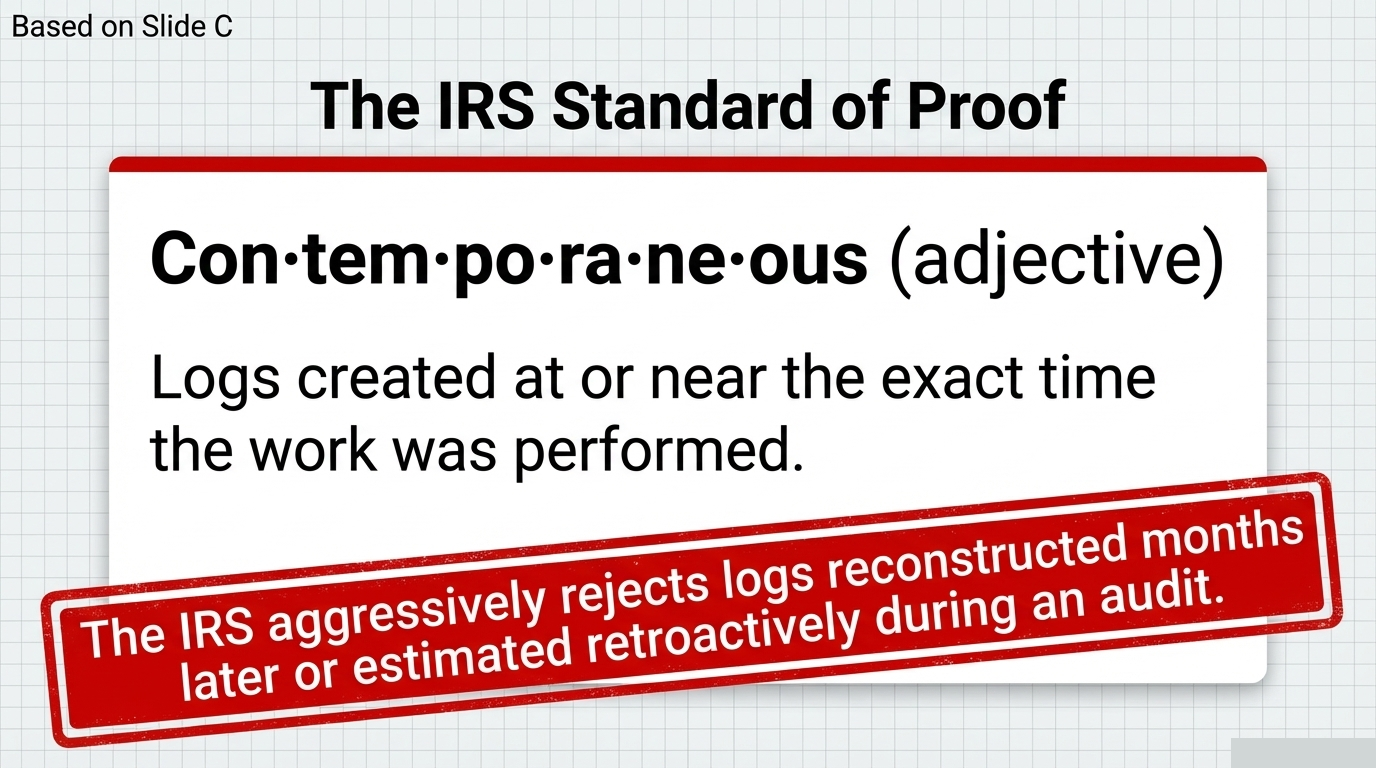

The IRS does not prescribe a specific format, but they want contemporaneous records — logs created at or near the time the work was done, not reconstructed months later. Your documentation should include:

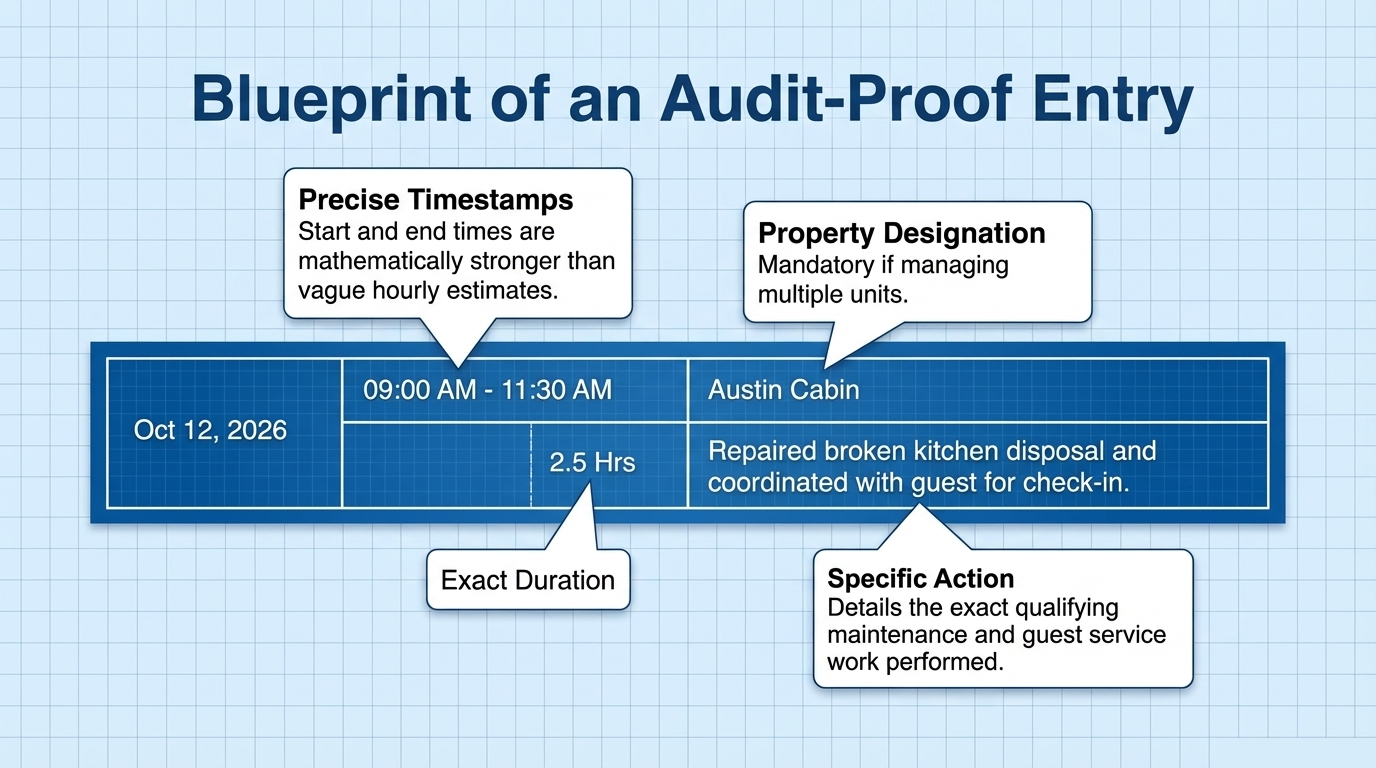

- Date of the work

- Description of what you did

- Hours spent (start and end times are stronger than estimates)

- Property the work was for

Every entry should answer four questions: when, how long, which property, and what exactly did you do?

Every entry should answer four questions: when, how long, which property, and what exactly did you do?

A single bulletproof entry: date, start/end times, property, and a specific description of the work performed.

A single bulletproof entry: date, start/end times, property, and a specific description of the work performed.

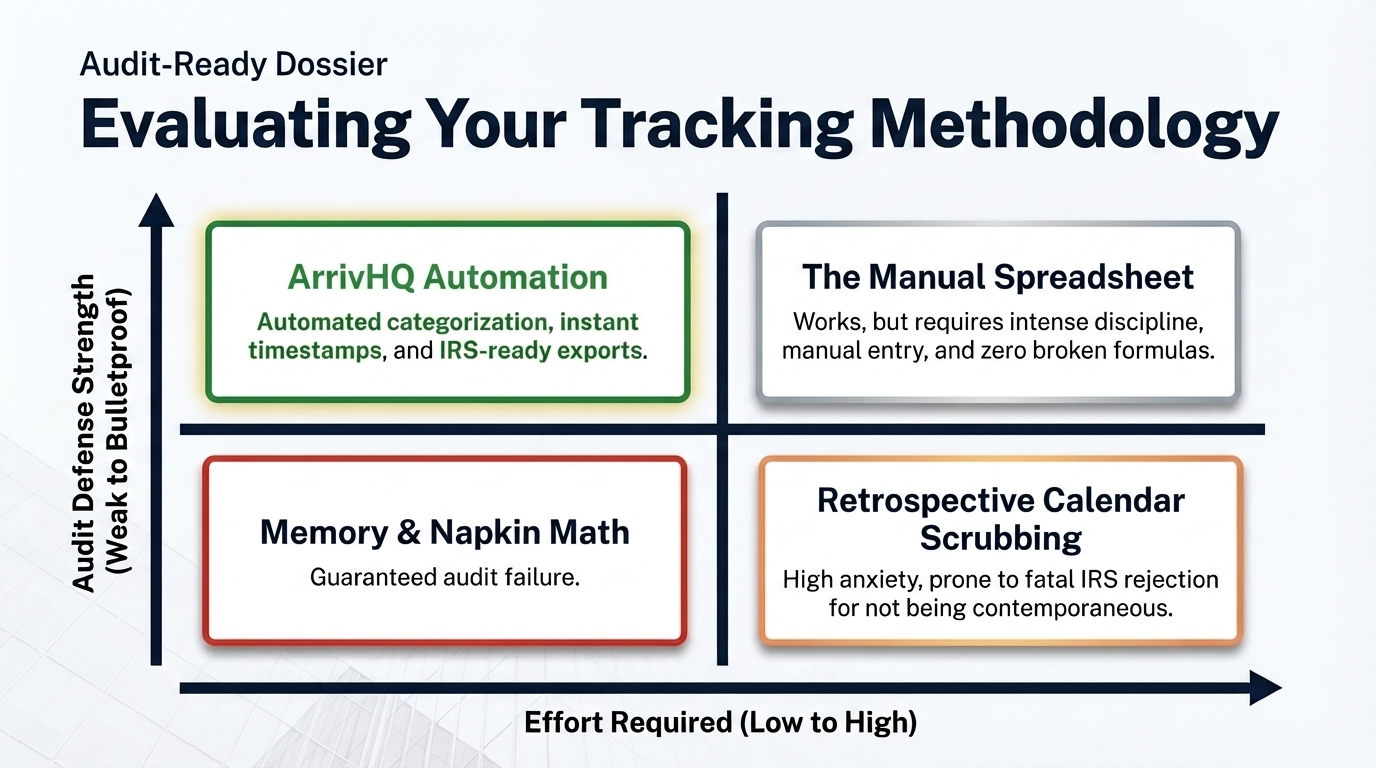

A spreadsheet works. A dedicated tool like ArrivHQ works better — it timestamps entries as you log them, categorizes activity types, and produces audit-ready exports.

Spreadsheets require you to defend their integrity. Dedicated tools generate proof as you work.

Spreadsheets require you to defend their integrity. Dedicated tools generate proof as you work.

ArrivHQ automates the three pillars of audit-proof documentation: timestamps, categorization, and exports.

ArrivHQ automates the three pillars of audit-proof documentation: timestamps, categorization, and exports.

The audit reality

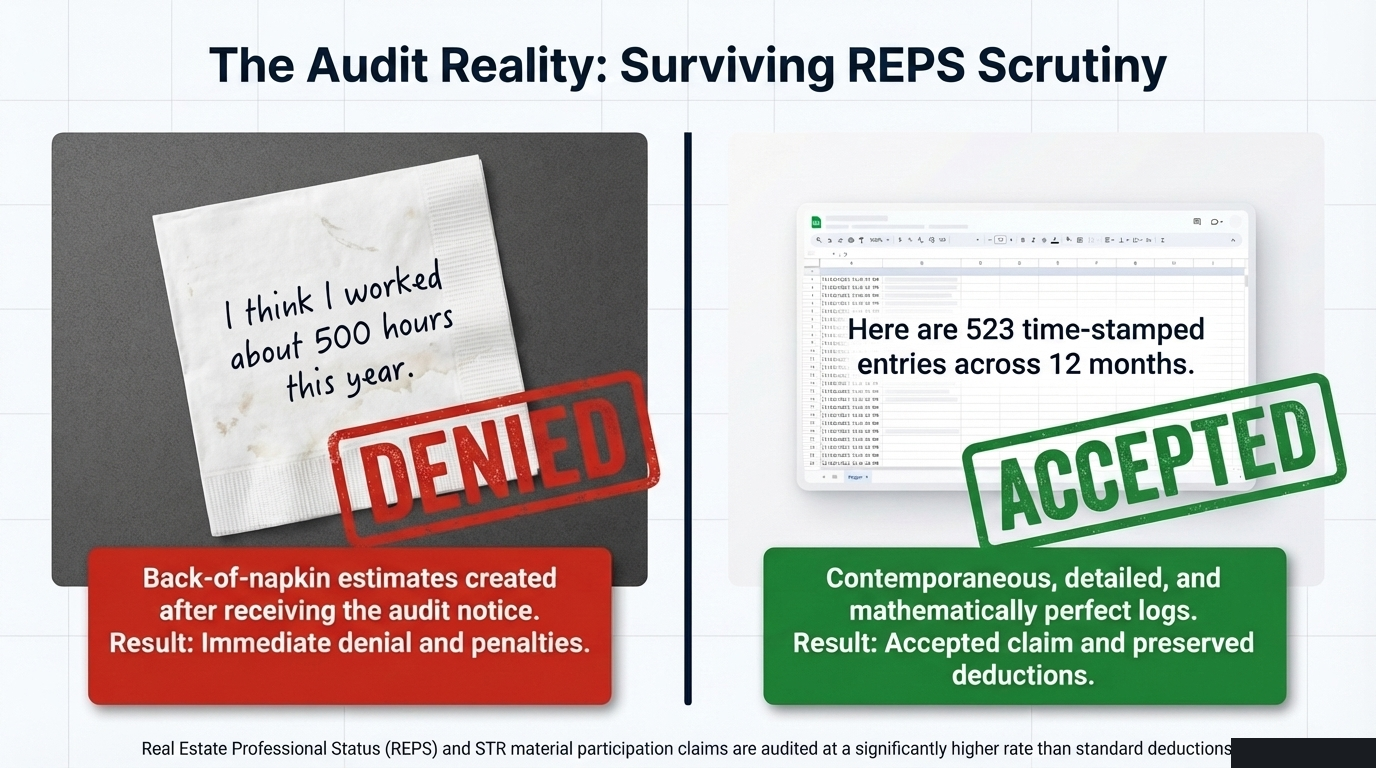

The IRS audits REPS claims at a higher rate than most other deductions. When they do, they ask for your log. If you have 500+ hours of detailed, contemporaneous entries, you are in a strong position. If you have a back-of-napkin estimate created during the audit, you are not.

The difference between "I think I worked about 500 hours" and "here are 523 time-stamped entries across 12 months" is the difference between an accepted claim and a denied one.

The moment you are audited, the very first request is your time log. Make sure it tips the scale.

The moment you are audited, the very first request is your time log. Make sure it tips the scale.

Start tracking now

Every hour you work on your STR and fail to log is an hour you cannot claim later. Start logging today — even if tax season feels far away. The hosts who survive audits are the ones who built the habit early.

Missing any single variable invalidates the formula. Every hour you work on your STR and fail to log is an hour you cannot claim later.

Missing any single variable invalidates the formula. Every hour you work on your STR and fail to log is an hour you cannot claim later.

Curious whether your hours put you on the active or passive side of the line? The free STR Tax Calculator estimates where you land against the IRS participation thresholds in about a minute.